Regulatory Diagnostic Toolkit for Digital Financial Services

In 2016, the UNSW Digital Financial Services Diagnostic Team (UNSW DFS Diagnostic Team), in collaboration with UNCDF, piloted the application of a Regulatory Diagnostic Toolkit (RDT) for digital financial services (DFS) in Solomon Islands. The RDT enables regulators to assess their regulatory environment in view of their objectives for DFS.

In many emerging countries the introduction of DFS has led to impressive advances in financial access. However, DFS present several challenges to regulators. How can a competitive DFS ecosystem be fostered to support improved products, prices and innovation? How can consumers be protected? How can customers’ funds be safeguarded against provider illiquidity or insolvency? And how does a regulator meet these challenges without stifling innovation and within existing technical and capacity resource constraints?

The RDT provides financial regulators with the clarity, perspective and structure needed to respond to these challenges. In applying the RDT we begin with an assessment of the current market situation and the regulator’s objectives for it. The RDT then provides a framework for regulators to analyse their regulatory regimes to identify barriers to the growth, or gaps in the regulation, of DFS or gaps in data-driven evidence underpinning the policy development process.

The RDT provides an objective means to assess regulatory frameworks and identify the aspects of those frameworks that may need review and adjustment. It assists regulators to optimise their regulatory capacity by prioritising and allocating regulatory resources in line with their objectives for market development.

The RDT aims to support regulators to move towards current international best practices such as those identified by the Global Partnership for Financial Inclusion, the Consultative Group to Assist the Poor, the Better Than Cash Alliance (BTCA), the Alliance for Financial Inclusion and other organisations active in this field. To this end an expected outcome of using the RDT is an improved capacity of regulators to promote optimal linkages among financial inclusion, financial stability, financial integrity and consumer protection.

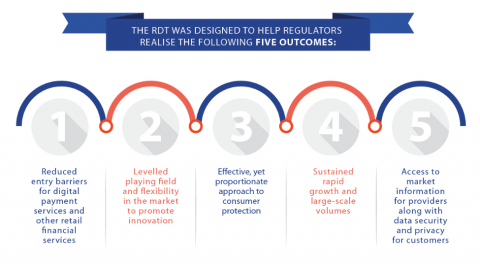

The RDT is a support for broader DFS ecosystem diagnostics such as the BTCA’s Ecosystem Diagnostics Toolkit. The RDT provides an analytical framework for conducting an improved policy development process which is firmly grounded in data-driven evidence-based research. The goals of this analytical framework can be summarised as:

- Reduced barriers to entry for digital payment services and other retail financial services;

- A level playing field and flexibility in the market to promote innovation;

- An effective yet proportionate approach to consumer protection;

- Sustained rapid growth and large scale volumes; and

- Access to market information for providers while ensuring security and privacy of customer data.

Having regard to these outcomes, the RDT contains seven subject domains which capture the many regulatory issues connected to DFS, including market conduct, prudential regulation, payments oversight, competition and privacy.

Each subject domain includes a subsidiary list of issues for regulators to consider when assessing how well their regulatory regime supports the development of the DFS ecosystem as envisaged by the regulator. Regulators are not expected to address the issues under each subject domain comprehensively. Rather, the subject domains provide regulators with a structured approach to assess their regime such that the main regulatory issues connected with DFS are considered and not inadvertently overlooked.

The seven subject domains are:

- Regulatory Architecture

This domain aims to provide an overview of the country’s DFS regulatory regime and helps identify and assess factors that give rise to barriers to the adoption, or gaps in the regulation, of DFS in relation to regulatory mandate, capacity and coordination.

- Building the Ecosystem

This domain examines the regulator’s intention and capacity to implement enabling regulation so as to support a sustainable DFS ecosystem. The dimensions include competition, innovation, consumer demand, financial literacy, interoperability, partnerships, and public access to market data.

- Protection of Funds

This domain evaluates whether the regimes for depositor and e-money funds protection effectively protect customers’ funds from insolvency, liquidity and operational risks.

- The Use of Agents

This domain examines the existing regulatory and contractual arrangements with regard to the use of agents, the allocation of liability, and the management of credit, liquidity and consumer risk that may arise among the provider, agent and customer.

- Consumer Protection

This domain assesses the effectiveness of the country’s financial consumer protection framework, considering regulatory mandate, industry codes, product disclosure, recourse mechanisms, use of agents and digital delivery of financial services. It is expected that in emerging markets a proportionate approach is taken, which means one that takes into consideration local context and the cost of the framework for regulators, providers and consumers are proportionate to the risks.

- AML/CFT

This domain evaluates how well the country is doing in terms of balancing the implementation of proportionate anti-money laundering/countering the financing of terrorism (AML/CFT) measures and the promotion of financial inclusion. Dimensions assessed include the use of a risk-based approach, the adoption of simplified Consumer Due Diligence (CDD), transaction monitoring and reporting, and new approaches to AML/CFT.

- Data Privacy

This domain reviews the country’s regulatory and contractual mechanisms for protection of customers’ data and privacy. Four dimensions are considered: the rights of individuals to privacy and data protection; the sharing of customers’ financial information among financial services providers; the use of customers’ credit information; and consumer redress mechanisms for misuse of data and infringement of privacy.

The RDT does not seek a generic approach to the regulation of DFS across the globe. Regulations work best when they are responsive and specific to the needs and realities of a country. Each country will have views on how its DFS ecosystem should develop which will shape their regulatory regimes. This local context is important. The assessment using the RDT must align with the current market context, the regulator’s vision and objectives given that market context, and the local definition of success.

Through the emphasis placed on data/evidence gathering, we expect the application of the RDT will, in close collaboration with other donor stakeholders, be able to help the regulator decide which of the seven domains it might best address first. The diagnostic exercise can also serve as an analytical basis to assist donor stakeholders to reach consensus on the priorities of different regulatory issues facing the country.

Lessons learned from pilot work suggest that early and extensive collaboration among domestic regulators, consultants and local champions from international donor agencies promotes the diagnostic process itself. Collaboration underpins the process of domestic regulators understanding and engaging in the RDT process and the recommendations that emerge from it. While the objective is to make the RDT available as a self-assessment tool, it would benefit from being implemented with support from external consultants or local specialists of interational development partners. International support also gives the process sufficient drive and acknowledges the technical and resource constraints faced by most regulators in emerging markets.

The RDT will be refined and adjusted over time. The document is available for public use and we welcome feedback on its continued development.